Face Mask,Earloop Surgical Mask,Earloop Face Mask,Disposable Earloop Face Mask QD Cloudy Inernational Pre Ltd , https://www.qdcloudy.com

Abstract: 1. The folk investment has fallen on the cliff. Private investment is mainly private, individual and collective enterprise investment, which is corresponding to state-owned enterprise investment and foreign enterprise investment. Before 2016, the growth rate of private investment has been higher than the growth rate of solid investment in the whole society. Since entering 2016, private investment has begun to stall and is significantly lower than the growth rate of solid investment in the whole society. In June, the growth rate of private investment in the month fell to -0.01%.

2. Private investment is mainly distributed in three major areas: manufacturing, real estate and labor-intensive low-end services (such as wholesale and retail and accommodation and catering). Private investment accounts for 81% and 71% respectively in the manufacturing and real estate sectors. Most of the service industry has serious regulations, and the proportion of state-owned investment accounts for 60%-80%. This also explains why the development of China's service industry is seriously lagging behind, the international competitiveness is low, and there is a huge trade deficit.

3. A new round of national advancement in the investment field. 1) Real estate industry: The central enterprises are eager to throw thousands of gold and land, and the private enterprises are frequently forced to retreat. The difference in the comprehensive financing cost between central enterprises and private enterprises determines the dominant position of central enterprises in the battle for land. 2) Manufacturing: Local governments endorse credit for state-owned enterprises, and private enterprises are forced to withdraw because of discrimination. The essence of the market mechanism is the survival of the fittest, the marketization, and the advantage of mergers and acquisitions. However, in the area of ​​overcapacity in China, in recent years, local governments have often cited cases of endorsement of credits for state-owned enterprises, which undermines the market competition mechanism. A large number of state-owned enterprises have become zombie enterprises, and they are not dead. 3) Service industry: State-owned monopoly administrative control, private investment encounters “glass door†and “spring doorâ€. With the climax of the upgrade of the residential line, the future consumption and service industry will usher in great development. 4) Reform of state-owned enterprises: bigger and stronger. 5) Private investment under the “national advancement and retreatâ€: go abroad. Due to the limited domestic private capital investment, the high cost of capital, and the high cost of the system, private enterprises began to seek overseas capital and investment opportunities. Since some industries do not allow private investment to enter, but allow foreign capital to enter, many private investors have gone through the ODI way to avoid the "spring door" and "glass door" as foreign capital.

4. A new round of national advancement in the financing field. 1) Financing structure of private investment: The problem of financing is difficult. Comparing the financing structure of Sino-US SMEs, China's private enterprises are highly dependent on endogenous financing (including their own capital and retained earnings), accounting for up to 60%, while the United States only has 30%; Chinese private enterprises borrow from banks, issue The ratio of bonds and equity financing is much lower than that of the United States. The “other†China accounts for nearly 20% of the total, which may include higher-cost private lending. 2) Identity discrimination and financial repression of private enterprises applying for loans. The proportion of private loans from Chinese banks (20%) is much lower than that of similar foreign companies (42%). For SMEs with less than 100 employees, the possibility of applying for a bank loan is more than 50%. 3) Bond default and credit risk premium: State-owned enterprises have implicit government guarantees and private enterprises are discriminated against. In the first half of 2015 and the first half of 2016, the coupon rate of bond issuance, central enterprises and local state-owned enterprises fell by 52bp and 73bp, while private enterprises only dropped by 27bp.

5. Over the past 30 years of reform and opening up, “national retreat and advancement†has promoted efficiency improvement. A new round of “national advancement and retreat†means that the efficiency of resource allocation in the whole society has declined. Since the reform and opening up, the general trend has been the retreat of the country. The proportion of the state-owned industrial economy has dropped from 77.6% in 1978 to 20.69% in 2008, which has promoted the efficiency of resource allocation. In the past few times, the retreat of the country has led to a decline in the efficiency of resource allocation. Private enterprises are more efficient than state-owned enterprises. Now private enterprises that can make money do not invest, and state-owned enterprises that continue to lose money continue to expand their territory. From January to June 2016, among industrial enterprises above designated size, investment in state-owned, collective, joint-stock, foreign-invested and private enterprises increased by -8%, -1.1%, 7.6%, 5%, and 8.8%, respectively.

6. Prevent a new round of national advancement and retreat. 1) For enterprises in the field of excess capacity, state-owned enterprises and private enterprises should treat them equally, compete fairly, and survive the fittest. Prevent state-owned enterprises from using the ownership of the system to obtain loans, debt-to-equity swaps, and reverse the elimination of private enterprises. 2) In addition to justifiably strengthening the state-owned enterprises, the reform of state-owned enterprises must also be bold and strong to become a better private enterprise and create a level playing field. In the end, the state-owned enterprises and private enterprises can be bigger and stronger, the market has the final say, the government can not be a referee, this is the basic spirit of the market economy and reform and opening up. 3) Local governments may not endorse credit for state-owned enterprise platforms, which violates the principle of fair competition in the market economy. 4) Strengthen the supervision of the phenomenon of state-owned enterprises to fight the land and suppress the asset price bubble. 5) Relaxation of service industry regulation. China's success in the past 30 years is the success of manufacturing openness, and the success of the next 30 years will be the success of the service industry. In recent years, the service industry has put a living piece, such as the Internet and the media. The areas that have not been released have been seriously lagging behind, such as finance and sports. 6) Large-scale reduction of corporate income tax, personal income tax, etc., and simplify the collection process, so that benefit the people, the effect is long-lasting, and significantly improve the company's expectations for the future. 7) Strengthen the protection of private property rights. Long-term investment will only be made if the company has long-term stable expectations. 8) Establish new cadre assessment and incentive mechanisms. In the past, local GDP championships were a major engine of China's high economic growth. In recent years, officials have been widely absent, and may be related to the uncertainty of the new assessment and incentive mechanism. After the dilapidation, it is necessary to establish a new one. In the future, it is possible to establish a new cadre assessment mechanism for comprehensive GDP, employment, and innovation. 9) The most fundamental thing in reform is to move property rights. In the 1980s, the household contract responsibility system was adopted, and in the 1990s, the state-owned enterprises in the joint-stock system were arrested. The most fundamental problem in the existence of state-owned enterprises is that the incentives caused by unclear property rights are not in place, which in turn leads to inefficiency.

table of Contents:

1 2016 private investment cliff-like decline

1.1 Private investment stalls 1.2 Industrial distribution of private investment

2 A new round of national advancement in the investment field

2.1 Real estate industry: the central enterprises are arrogant and arrogant, and the private enterprises are frequently forced to retreat. 2.2 Manufacturing: Local governments endorse credits for state-owned enterprises, private enterprises are forced to withdraw because of discrimination, and bad money drives out good debts. 2.3 Service industry: state-owned monopoly administration Control, private investment encounters "glass door" and "spring door"

2.4 State-owned enterprise reform: bigger and stronger, better than the private investment under the “national advancement and retreatâ€: go abroad

3 A new round of national advancement in the financing field

3.1 The financing structure of private investment: the problem of financing is difficult. 3.2 The identity discrimination and financial repression of private enterprises applying for loans 3.3 Bond default and credit risk premium: State-owned enterprises have implicit government guarantees, and private enterprises are discriminated against.

4 Reform and opening up over the past 30 years, “national retreat and advancement†has promoted efficiency improvement. A new round of “national advancement and retreat†means that the efficiency of resource allocation in the whole society has declined. 5 Preventing a new round of national advancement and retreat

text:

Private investment is mainly private, individual and collective enterprise investment, which is corresponding to state-owned enterprise investment and foreign enterprise investment. This year's private investment in the cliff-type decline has aroused widespread concern and discussion from all walks of life. The Party Central Committee and the State Council have repeatedly supervised and promoted private investment. The decline in private investment and the rise of state-owned investment is essentially a new round of national advancement.

The practice in the past 38 years of reform and opening up shows that in the competitive field, private enterprises are more efficient than state-owned enterprises. The new round of national advancement and retreat indicates that the investment efficiency of the whole society is dropping drastically.

1 2016 private investment cliff-type decline 1.1 private investment stall

The proportion of private fixed assets investment in the fixed assets investment of the whole society exceeded 50% in March 2010, and has remained above 60% since 2012. Private investment has become the main force of fixed asset investment in the whole society. However, since 2011, due to cyclical, institutional and structural factors, private investment has begun to decline. At the same time, the government began to increase infrastructure investment in order to hedge the downward pressure on the economy, and the growth rate of private investment and government investment began to differentiate. .

Before 2016, although the growth rate of private investment declined, its growth rate has been higher than the growth rate of fixed assets investment in the whole society. In 2013, the growth rate of private investment was 23.1%, which was 3.5 percentage points higher than that of the whole society. In 2014, the growth rate of private investment was 18.1%, which was 1.4 percentage points higher than that of the whole society. In 2015, the growth rate of private investment was 10.1%, higher than the investment of the whole society. 0.1 percentage points. However, after entering 2016, private investment began to stall. The cumulative increase in private investment in February 2016 was significantly lower than that of fixed asset investment, and the gap between the two was gradually increasing. By June of this year, the year-on-year growth rate of private investment fell to -0.01%, entering a negative growth range.

Before analyzing the reasons, we need to first find out which areas of private investment have gone wrong in order to find the root cause of the problem.

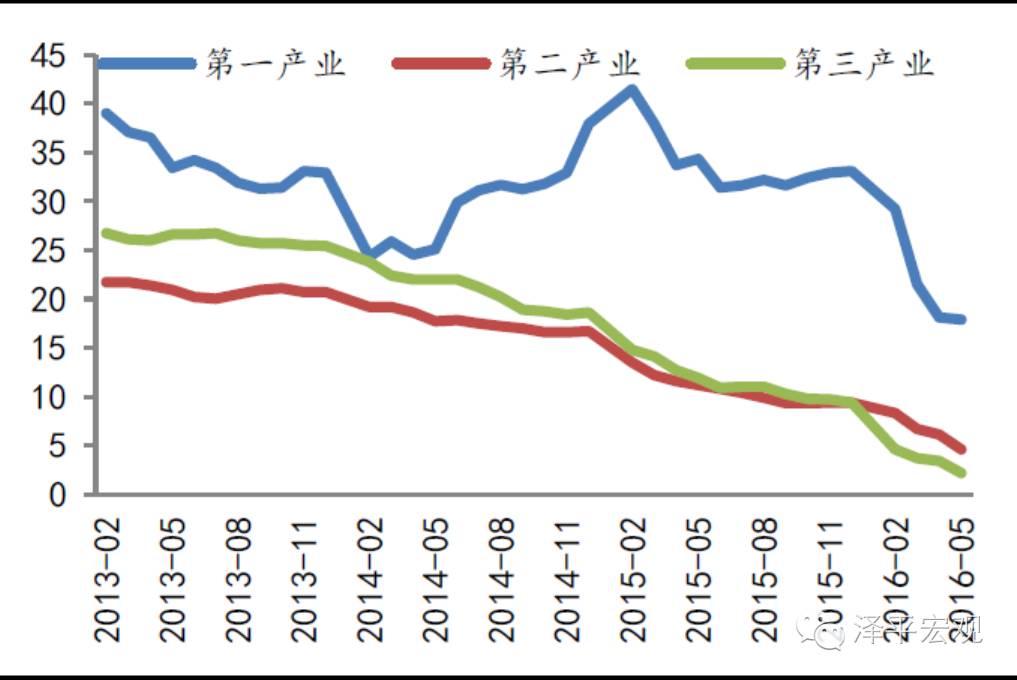

From the perspective of three industries, the decline in private investment since 2016 is mainly dragged down by the secondary and tertiary industries. From January to June, the investment in private fixed assets of the first, second and third industries increased by 19.7%, 2.8% and 1.6% respectively, which was 1.8, -1.8 and -0.6 percentage points respectively from January to May.

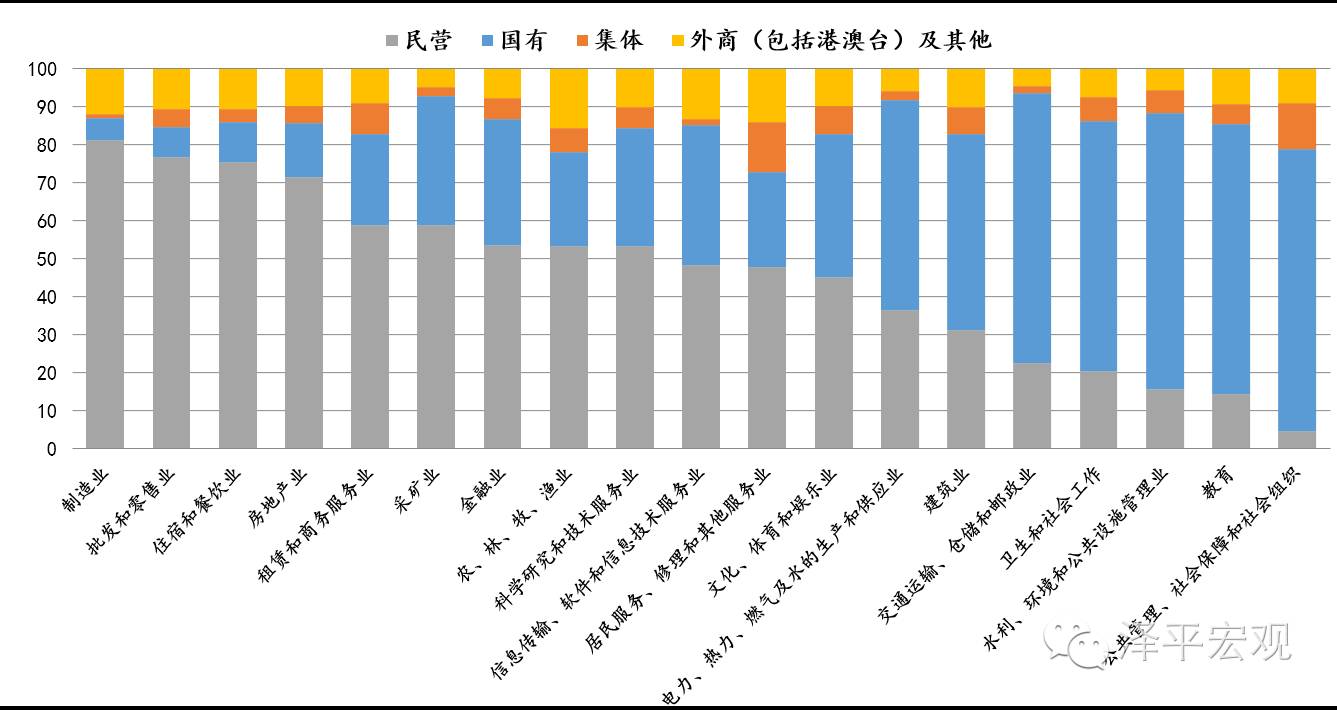

From the ownership structure of fixed asset investment (in 2014 data), private investment is mainly distributed in three major areas: manufacturing, real estate and labor-intensive low-end services (such as wholesale and retail and accommodation and catering). Among them, private investment accounted for 81% and 71% respectively in the manufacturing and real estate sectors. Most of the service industry has serious regulations, and the proportion of state-owned investment accounts for 60%-80%. This also explains why the development of China's service industry is seriously lagging behind, the international competitiveness is low, and there is a huge trade deficit.

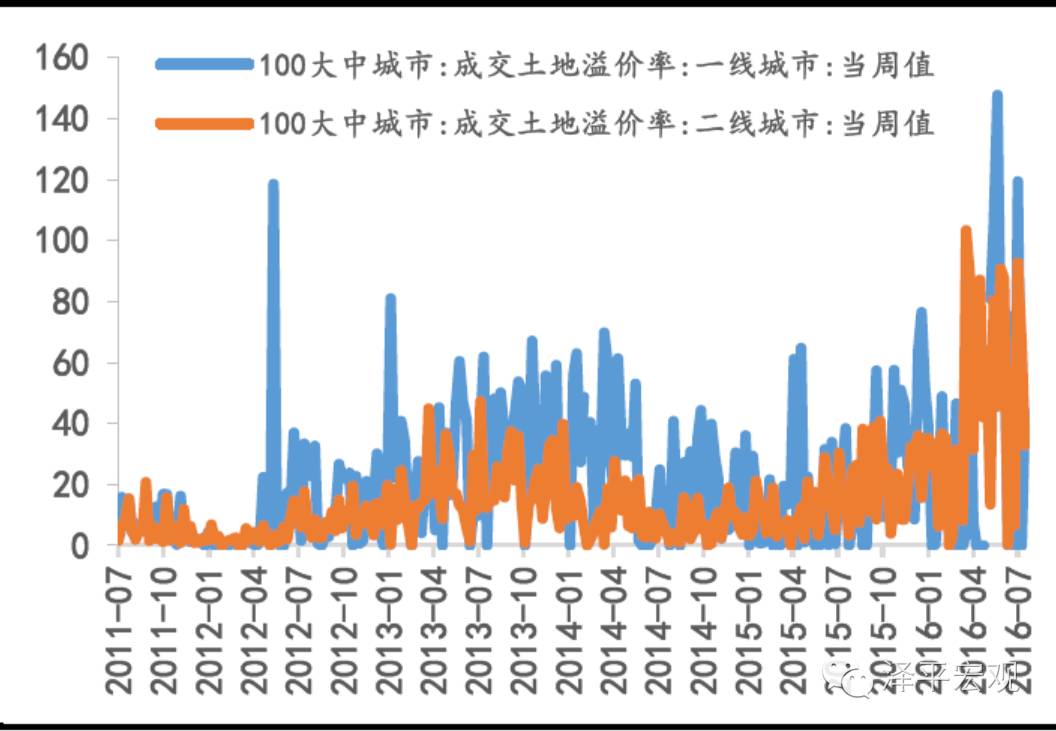

From January to May 2016, 105 high-priced plots with a total land market price of more than 1.5 billion yuan were sold at a total price of 328.82 billion yuan, of which 52 were obtained by state-owned enterprises, with a total turnover of 178.58 billion yuan, accounting for 54%. Among them, Cinda, OCT, China Merchants Shekou (14.960, 0.00, 0.00%), Dianjian Real Estate, Luneng Group, Gezhouba (7.110, 0.00, 0.00%), Poly, China Railway, China Metallurgical and other central enterprises have produced 15 land kings. . The most outstanding performance is Cinda Real Estate (4.970, 0.00, 0.00%). Since July 2015, Cinda Real Estate has added 10 new plots through public bidding, of which 7 are landlords.

Different from previous years, the threshold of the king of the earth has increased. In 2016, the land transaction premium rate jumped to a new level, especially in first-tier cities. The transaction premium rate of “Diwang†mostly exceeds 100%, and a large part exceeds the level of 200%. For example, in the auction of Zhoupudiwang on June 1, a total of 7 of the 24 real estate enterprises were central enterprises, and finally Cinda The transaction premium rate was 306.53%. In the past, the 100% premium rate is rare. For example, on October 30, 2015, China Jinmao refreshed the local total price of “land king†in Hangzhou with a total transaction price of 3.884 billion yuan, with a premium rate of only 66.05%.

The bidding behavior of central enterprises in the land auction without cost is obviously contrary to the market law and violates the market economy foundation of fair competition. The difference in the comprehensive financing cost between central enterprises and private enterprises determines the dominant position of central enterprises in the battle for land. Compared with private housing enterprises, central enterprises and state-owned enterprises rely on state-owned identity financing to make it easier and cheaper.

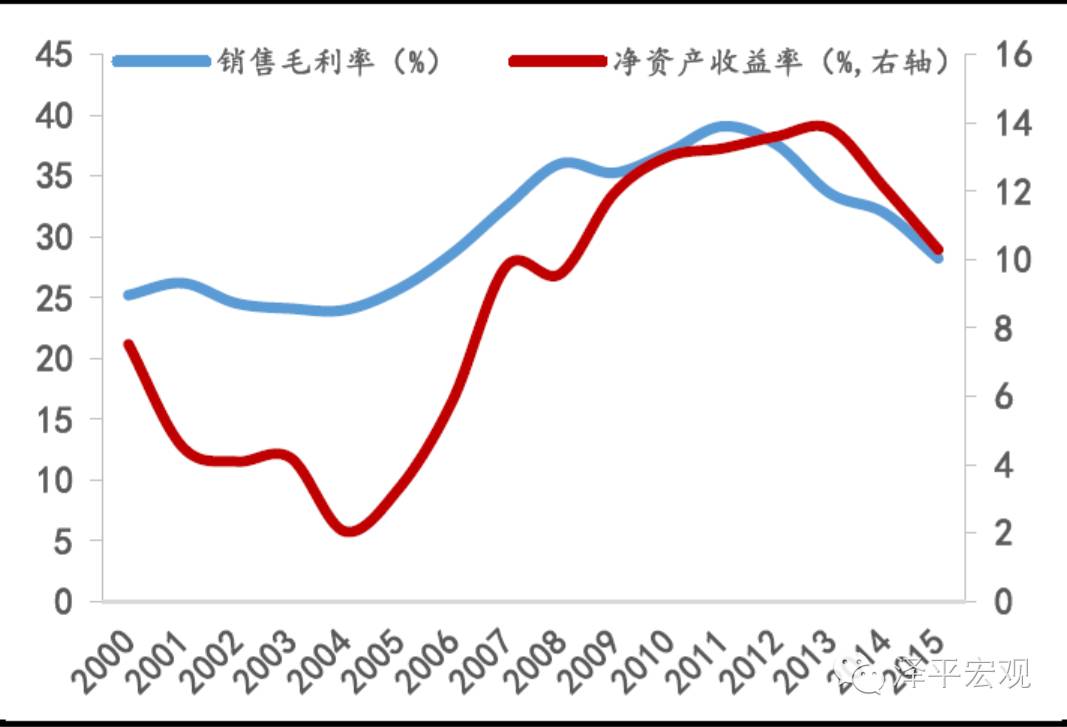

With the peak of the real estate cycle, the ROE of the entire industry began to decline rapidly. The ROE of listed homes in 2015 fell to 10.3%. The 2016 mid-year report showed that the ROE further fell to 9.0%. With the further reduction of profit space in the future, the living space of private housing enterprises will be further squeezed by state-owned enterprises.

The essence of the market mechanism is the survival of the fittest, market-oriented clearing, and the integration of disadvantaged enterprises through mergers, improve industry concentration, optimize resource allocation efficiency, and promote industrial upgrading. However, in the field of overcapacity in China, in recent years, local governments have often cited cases of endorsement of credits by state-owned enterprises, which have undermined the market competition mechanism. A large number of state-owned enterprises have become zombie enterprises, and they are not dead. This is a case of reform. "Regression". Private enterprises are in a situation of being discriminated against and forced to withdraw, which has led to bad money expelling good money and reverse elimination.

In the period of speed increase and shift, steel, coal, building materials, chemicals and other fields have already bid farewell to the era of high growth, and overcapacity has become prominent. However, in many overcapacity industries, state-owned enterprises are getting together and their profits are declining. They can only rely on new debts and old debts, and they are deeply mired in debt. Zombie enterprises are essentially Ponzi financing. However, due to considerations such as employment, GDP, and political achievements, local governments do not want state-owned enterprises to go bankrupt due to avoiding bad exposures. They are endorsed by state-owned zombie platforms, which is very common in recent years, such as returning to the planned economy. era.

In the first half of 2016, some state-owned enterprises began to default on bonds, and credit risks were highlighted. On July 25, the State Council issued the "Opinions on Deepening the Reform of Investment and Financing System", proposing that the pilot financial institutions hold corporate equity according to law, and the market interprets this as a pilot debt-to-equity swap. However, in practice, debt-for-equity swaps are only applicable to state-owned enterprises. The current debt-to-equity swap pilots are mainly in the coal and steel industries where state-owned enterprises are relatively high. Most of the enterprises that intend to withdraw from the debt-to-equity swap scheme are state-owned enterprises, such as Sinosteel and Northeast Special Steel in the steel industry. On July 5, Panjiang issued an announcement, and Panjiang Holdings has signed an equity restructuring agreement with the Guiyang Municipal Government to convert all of Huaneng Coking’s claims held by the former into equity.

When Zhou Xiaochuan studied the issue of debt-to-equity swaps in 1999, he mentioned that debt-for-equity swaps must be “the right medicineâ€, and not all companies are suitable for debt-for-equity swaps [1]. He believes that "the significance of debt-to-equity swaps is not mainly to reduce the interest burden, but more importantly, to increase the control of creditor banks, increase pressure on loans, and increase the influence of banks on corporate financial issues. Therefore, The substantive role of debt-to-equity swaps is to change the corporate governance structure within the enterprise and enable companies to accept severe or painful restructuring plans."

With the climax of the consumption upgrade of the residential area, the future consumption and service industry will usher in great development. However, the administrative control of "glass doors" and "spring doors" in the service sector has inhibited the entry of private investment. Private investment is concentrated in the general manufacturing and real estate industries, as well as in traditional service industries such as wholesale and retail, trade, catering, and private investment in the service industry is clearly insufficient.

The Provisional Regulations on Private Enterprises and the retail industry of 12 industries, 36 national planned commodities and 41 important industrial production materials as stipulated by the State Administration for Industry and Commerce, there are “limited access†cases for private enterprises. The main reasons are:

First, due to the existence of departments, industry monopolies and other discriminatory access policies, private capital has been difficult to enter the financial, insurance, securities, postal, communications, petrochemical, power and other industries.

Second, although some projects allow private capital to intervene, there are obvious unfair competitions, and some state-owned enterprises have long-term monopoly operations.

Third, in some areas, due to the complicated approval procedures and the harsh entry conditions, private capital is beyond reach.

Fourth, many industries are open to the outside world, but there is no clear statement on whether private investment is open, such as telecommunications and banking.

Some policy rules are also difficult to implement. For example, the rules of the China Banking Regulatory Commission stipulate that “the restrictions or other additional conditions for private capital to enter the banking industry should not be set separatelyâ€; on the other hand, it is mandatory to require the village banks to be owned by existing commercial banks. As a host bank, private capital cannot independently establish a village bank. Another example is the “36 private investment†regulations, which encourage private enterprises to actively participate in international competition, develop strategic resources, and establish an international sales network. However, the relevant departments stipulate that if the crude oil resources that private enterprises seek overseas are to be shipped to China, they must have a “schedule plan†for the two major oil companies, otherwise they will not be allowed to import. The unfair and opaque policies have greatly damped the willingness of private capital to invest.

2.4 State-owned enterprise reform: bigger and stronger

The guiding ideology of the current state-owned enterprise reform is to become bigger and stronger, and to prevent the loss of state-owned assets. Under this guiding ideology, how to promote the development of private investment has become an important issue.

2.5 Private investment under the “national advancement and retreatâ€: going abroad

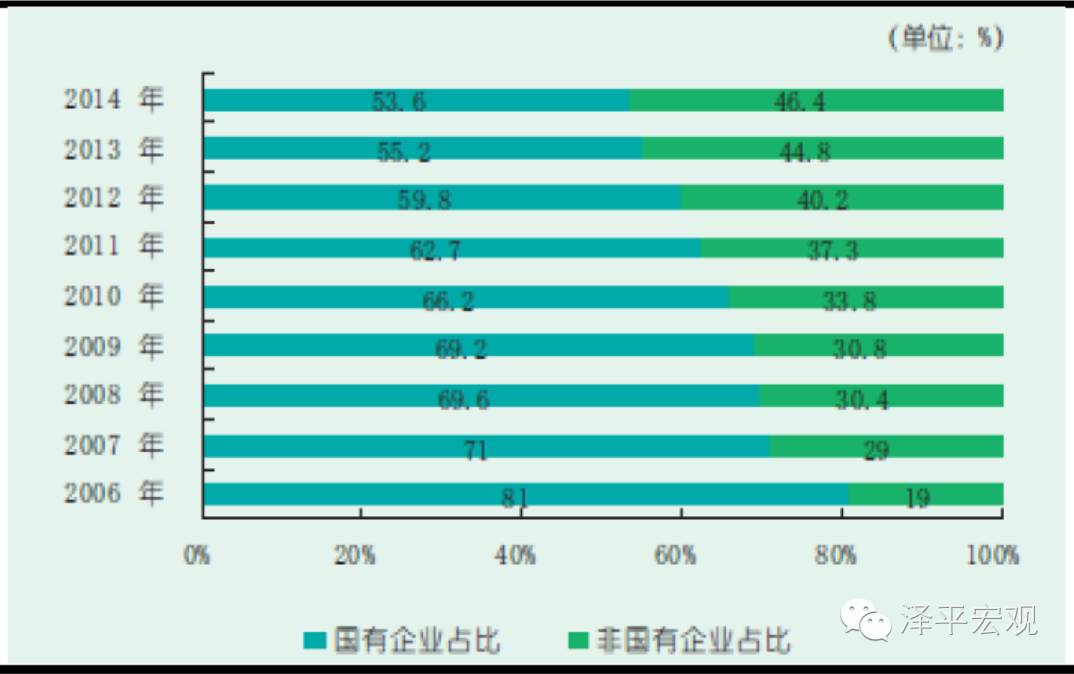

According to the statistics of China's Foreign Direct Investment Statistics Bulletin, the proportion of non-state-owned foreign investment has increased year by year, from less than 20% in 2006 to 46% in 2014.

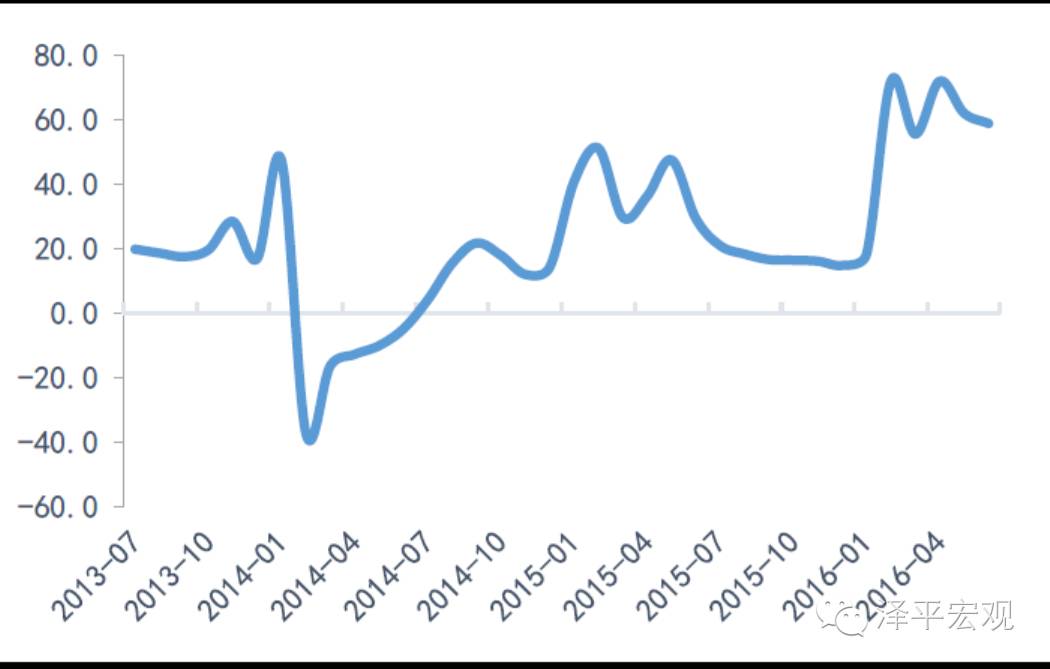

Due to the limited domestic private capital investment, high capital costs, and high institutional costs, private enterprises are encouraged to seek overseas capital and investment opportunities, and they can also enjoy the state's support policies for “going out†enterprises. At the same time, because some industries do not allow private investment to enter, but allow foreign capital to enter, so private investment through the ODI way to go out, to avoid the "spring door" and "glass door" as a foreign capital. In 2016, the growth rate of non-financial foreign direct investment rose linearly, which was significantly higher than the growth rate in 2015.

According to the Ministry of Commerce, in the first quarter, China’s direct investment in Hong Kong was US$20.68 billion, up 61% year-on-year, accounting for 51.6% of foreign investment in the same period; US investment was US$5.24 billion, up 2.6 times over the same period last year. The investment in ASEAN was 2.29 billion U.S. dollars, a year-on-year increase of 44%. The foreign investment in the above countries and regions accounted for more than 70% of the investment this year. Similarly, from January to May 2016, Shanghai had 643 foreign direct investment records, with a total foreign investment of US$30.098 billion, a year-on-year increase of 58.6%; the actual foreign investment was US$13.157 billion, a year-on-year increase of 228%.

The difficulty of financing small and medium-sized enterprises is a world phenomenon, especially in China. China's state-owned enterprises have received various preferential treatments for financing because of implicit government guarantees. The financing of small and medium-sized enterprises (mostly non-state-owned enterprises) not only has to bear higher costs, but also is difficult to apply. From the comparison of the financing structure of Sino-US SMEs, China's private enterprises are highly dependent on endogenous financing (including their own capital and retained earnings), which accounts for up to 60%, while the US counterpart is only 30%; The proportion of Chinese private enterprises from bank loans, bond issuance and stock financing is much lower than that of the United States. The “other†China accounts for nearly 20% of the total. This may include private lending with higher financing rates.

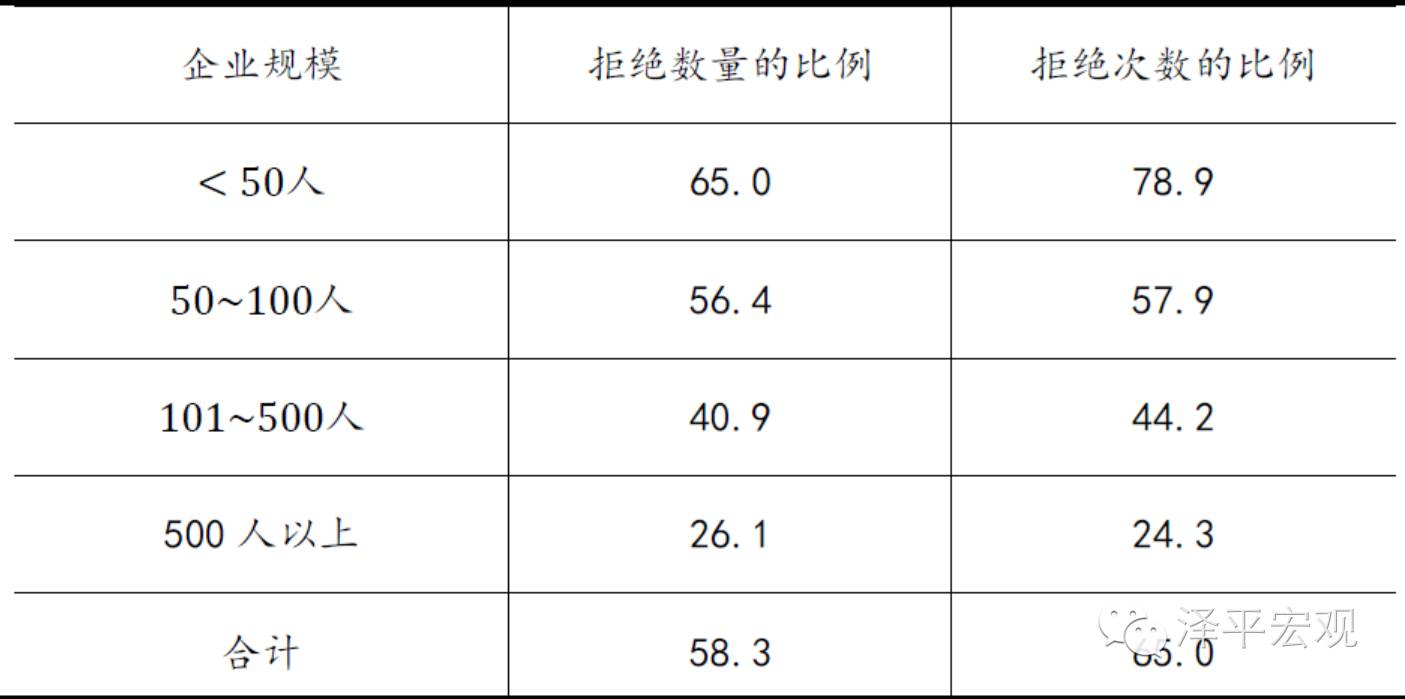

Chinese private enterprises have a relatively simple source of financing and rely heavily on endogenous financing. The proportion of private enterprises borrowing from banks (20%) is much lower than that of similar foreign companies (42%), and the actual demand is far from being met. For small and medium-sized enterprises with less than 100 employees, the possibility of applying for bank loans being rejected is more than 50%, and the problem of financing difficulties is far from being solved.

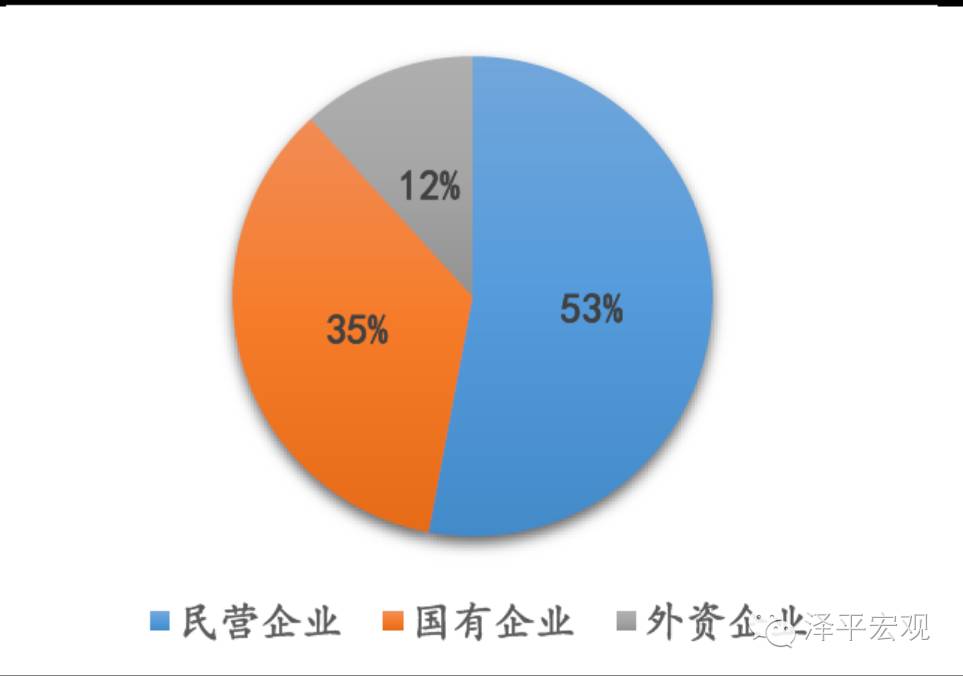

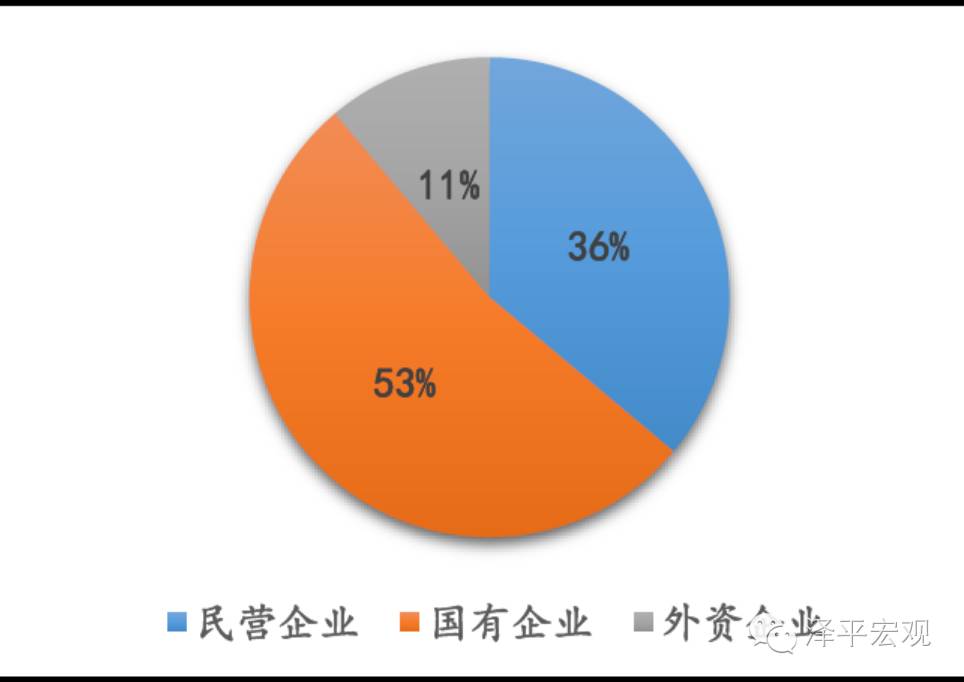

Credit risk events in the credit bond market have continued to increase since 2015. From the latest situation, the “high-rising time window†of the current credit default event is still continuing. In 2016, 53% of default bonds were private enterprises and 35% were state-owned enterprises. However, if we look at the default bond structure, we find that 53% of default bonds are issued by state-owned enterprises, while only 36% of default bonds are issued by private enterprises. That is to say, although private enterprises are more likely to default than state-owned enterprises, once state-owned enterprises lose the government's implicit guarantees, the default density is even greater.

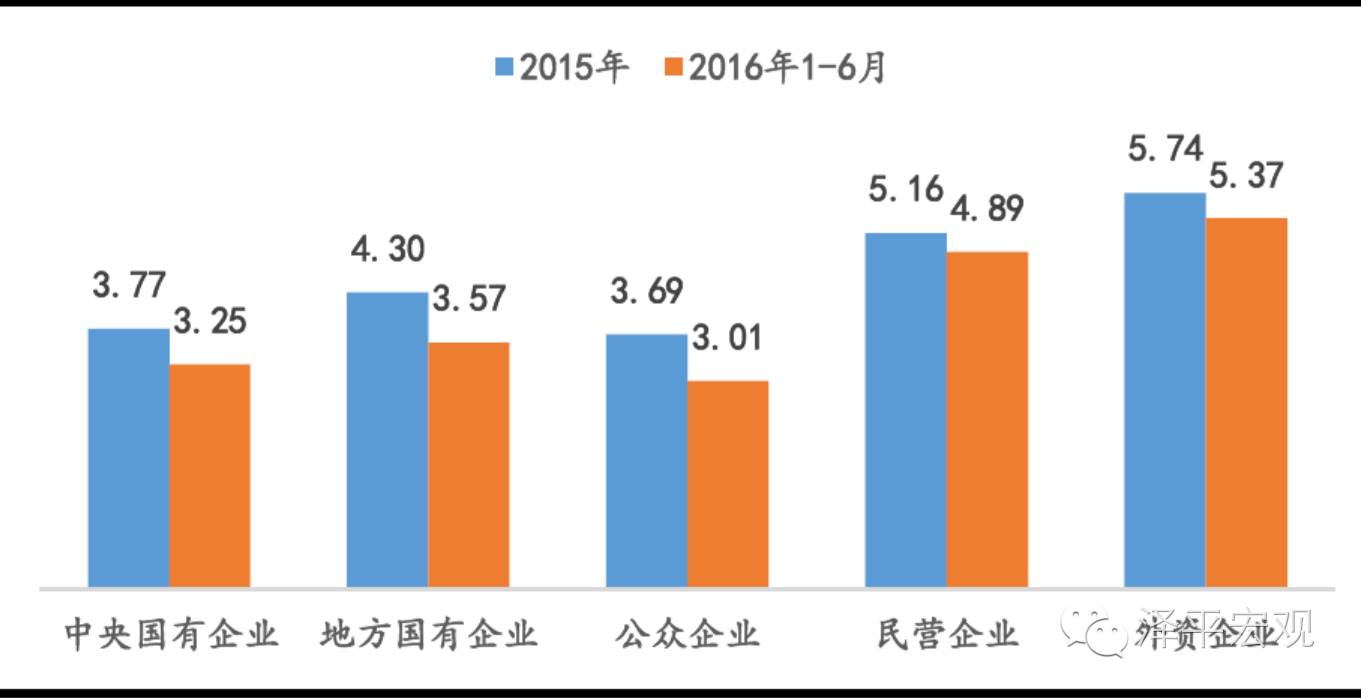

Based on the above findings, it can be speculated that in the absence of government implicit guarantees, the credit risk premium of state-owned enterprises in 2016 should be at least not lower than that of private enterprises of the same class. However, after comparing the coupon rates of private enterprises and state-owned enterprises in the first half of 2015 and 2016, it can be found that the coupon rates of central enterprises and local state-owned enterprises have dropped by 52 bp and 73 bp, and the coupon rate of listed companies has dropped by 68 bp, while private enterprise bonds have been issued. The coupon rate is only reduced by 27bp, which means that in the same macroeconomic environment, the same risk event will be faced. Ultimately, state-owned enterprises will survive because of the government's endorsement, and private enterprises may go bankrupt.

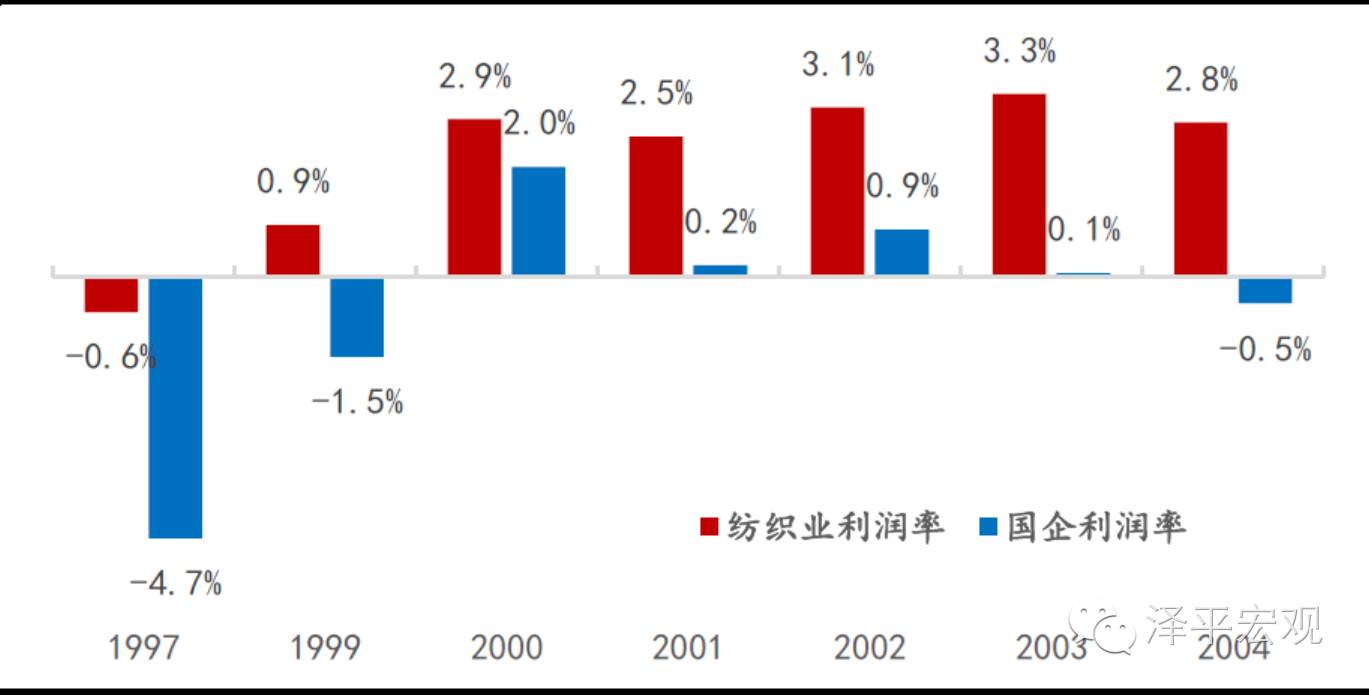

The general trend since the reform and opening up has been the retreat of the country and the promotion of the efficiency of resource allocation. Over the past 30 years, China’s ownership structure has undergone significant changes. The overall trend is that the country’s national economic growth has declined from 77.6% in 1978 to 20.69% in 2008, with an average annual decline of 1.86%. The proportion of the non-state-owned industrial economy has steadily increased. In particular, in 1998-2000, after the textile industry, which was a pillar industry, suffered serious losses in the 1990s, it quickly retired its excess capacity through state-owned enterprise restructuring, and the textile industry regained its vitality in the early 20th century.

In the past few times, the retreat of the country has led to a decline in the efficiency of resource allocation. The earliest phenomenon of “national advancement and civil retreat†appeared in the steel industry, including cross-regional restructuring of “Anshan, Ben, Panâ€, mergers between Tianjin Steel and Tianjin Iron and Steel, and state-owned Shandong Steel (2.420, which lost 1.285 billion yuan in half a year). 0.00, 0.00%) Jiang Ran reversed the acquisition of Rizhao Steel, which earned 1.8 billion yuan in half a year, using bank loans. These merger and reorganization cases were all inferior afterwards. Followed by the civil aviation industry, the state-owned China Aviation Group acquired East Star Airlines, the Eastern Airlines and Shanghai Airlines under the State-owned Assets Supervision and Administration Commission, Sichuan Airlines Holdings Eagle United Airlines. In the petrochemical industry, PetroChina, Sinopec and CNOOC have accelerated the merger of private gas stations, while extending their business upstream and downstream, leaving almost no living space for private enterprises.

The new round of "national advancement and civil retreat" means that the efficiency of resource allocation in the whole society has declined. The real estate industry has frequently seen the central government's efforts to fight for the land, and the local governments in the manufacturing sector have refused marketization for the state-owned enterprises and the state-owned monopoly administrative control in the service sector. The phenomenon of discrimination in the status of private enterprises in the financing field has caused more and more attention, discussion and reflection.

Private enterprises are more efficient than state-owned enterprises. Now private enterprises that can make money do not invest, and state-owned enterprises that continue to lose money continue to expand their territory. From January to June 2016, among industrial enterprises above designated size, the profits of state-owned holding companies fell by 8% year-on-year, the profits of collective enterprises fell by 1.1%, the profits of joint-stock enterprises increased by 7.6%, and the profits of foreign-invested enterprises from Hong Kong, Macao and Taiwan increased by 5%. Corporate profits increased by 8.8%.

First, for enterprises in the field of excess capacity, state-owned enterprises and private enterprises should be treated equally, fair competition, and survival of the fittest. Prevent state-owned enterprises from using the ownership of the system to obtain loans, debt-to-equity swaps, and reverse the elimination of private enterprises.

Second, in addition to the rationalization of state-owned enterprise reform, we must also strive to be bigger and stronger, better and better, and create a level playing field. In the end, the state-owned enterprises and private enterprises can be bigger and stronger, the market has the final say, the government can not be a referee.

Third, local governments must not endorse credit for state-owned enterprise platforms, which violates the fair competition rules of the market economy.

Fourth, strengthen the supervision of the phenomenon of state-owned enterprises to fight the land, and curb the asset price bubble.

Fifth, relax the regulation of the service industry. There are administrative controls and monopolization of state-owned enterprises in the service industry, resulting in serious development lag and low competitiveness. A large amount of consumption has gone abroad. In 2014, Chinese residents’ outbound travel expenses exceeded RMB 1 trillion. China's success in the past 30 years is the success of manufacturing openness, and the success of the next 30 years will be the success of the service industry. In recent years, the service industry has put a living piece, such as the Internet and the media. The areas that have not been released have been seriously lagging behind, such as finance and sports.

Sixth, implement large-scale tax cuts to benefit the people and improve the efficiency of resource allocation. During the supply-side reform period in the United States, the United Kingdom, Japan, and Singapore, the company reduced the corporate income tax and personal income tax on a large scale, and simplified the collection process. Although the short-term effect is not obvious, the effect is long-lasting and significantly improves the company's expectations for the future.

Seventh, strengthen the protection of private property rights. Long-term investment will only be made if the company has long-term stable expectations. Residents have long-term stable expectations and will continue to spend steady consumption.

Eighth, establish a new cadre assessment and incentive mechanism. In the past, local GDP championships were a major engine of China's high economic growth. In recent years, officials have been widely absent, and may be related to the uncertainty of the new assessment and incentive mechanism. After the dilapidation, it is necessary to establish a new one. In the future, it is possible to establish a new cadre assessment mechanism for comprehensive GDP, employment, and innovation.

Ninth, the most fundamental thing in reform is to mobilize property rights. Li Yining "China's reform failure may be the failure of price reform. The success of China's reform must depend on the success of ownership reform." Wu Jinglian "Institutions are greater than technology." In the 1980s, the household contract responsibility system was adopted, and in the 1990s, the state-owned enterprises in the joint-stock system were arrested. The most fundamental problem in the existence of state-owned enterprises is that the incentives caused by unclear property rights are not in place, which in turn leads to inefficiency.

The decline in private investment is essentially a new round of national advancement

Abstract Introduction: The decline in private investment and the rise in state-owned investment is essentially a new round of national advancement and retreat. The practice in the past 38 years of reform and opening up shows that in the competitive field, private enterprises are more efficient than state-owned enterprises. The new round of national advancement and retreat indicates that the investment efficiency of the whole society is dropping drastically. Summary: 1,...

Guide: The decline in private investment and the rise in state-owned investment is essentially a new round of national advancement. The practice in the past 38 years of reform and opening up shows that in the competitive field, private enterprises are more efficient than state-owned enterprises. The new round of national advancement and retreat indicates that the investment efficiency of the whole society is dropping drastically. Figure 1: Cumulative growth rate of fixed asset investment and private investment

1.2 Industrial distribution of private investment Figure 2: Cumulative share of investment in private assets in various industries

Figure 3: Accumulated year-on-year (%) of private investment in various industries

Figure 4: Ownership structure of China's fixed asset investment sub-sector in 2014 (%)

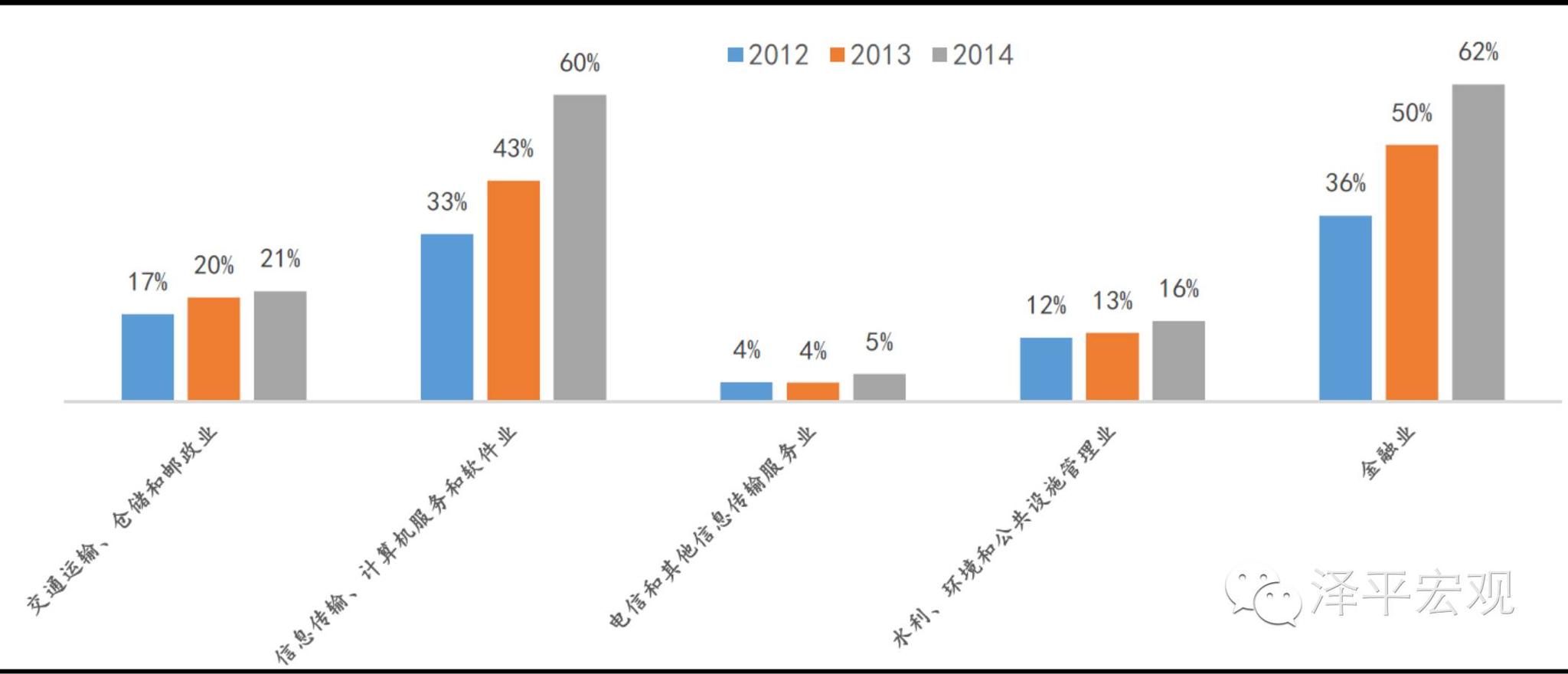

Figure 5: Proportion of private investment in state-owned investment in the tertiary industry in 2012-2014 (%)

2 A new round of investment in the field of national advancement of the people 2.1 Real estate industry: the central enterprises are eager to throw the king, the private enterprises are frequently forced to retreat Figure 6: The land transaction premium rate in 2016 has risen markedly

Figure 7: The profit margin of the real estate industry declines

Figure 8: The highest total transaction price of 50 single land in 2016

2.2 Manufacturing: Local governments endorse credits for state-owned enterprises, and private enterprises are forced to withdraw because of discrimination. Figure 9: The proportion of state-owned enterprises in fixed assets investment in overcapacity industries

2.3 Service industry: State-owned monopoly administrative control, private investment encounters “glass door†and “spring door†Figure 10: ODI stocks in both state and non-state enterprises

Figure 11: Non-financial foreign direct investment cumulative year-on-year (%)

3 A new round of national advancement in the financing field 3.1 The financing structure of private investment: the problem of financing is difficult Table 12: Sino-US SME financing structure (%)

3.2 Identity discrimination and financial repression of private enterprises applying for loans Table 13: Approval of bank applications for SME loans (%)

3.3 Bond default and credit risk premium: state-owned enterprises have implicit government guarantees, and private enterprises are discriminated against Figure 14: Corporate ownership structure for 2016 bond defaults

Figure 15: Bond structure for default in 2016

Figure 16: Comparison of coupon rates for bond issuance for 2015-2016 (%)

4 Reform and opening up over the past 30 years, “national retreat and advancement†has promoted efficiency improvement. A new round of “national advancement and retreat†means that the efficiency of resource allocation in the whole society has declined. Figure 17: Profits return to normal after the textile industry “returns from the countryâ€

5 Preventing a new round of national advancement