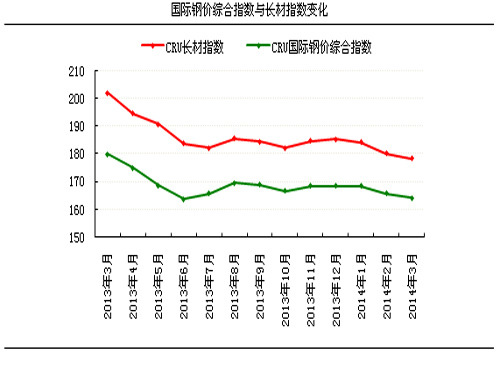

In March, the decline in construction materials continued, and the decline narrowed. Among them, the price of snails in Central China rose slightly. High inventory levels, slow start-up of demand, and financial pressure at the end of the quarter. The combined effect of these three factors will continue to constrain steel prices, and merchant shipments will dominate the market. The number of steel mills overhauled during the month increased, and crude steel production stopped rising and falling. Moreover, demand in the steel market picked up seasonally. The pace of purchases by intermediate dealers and terminals accelerated slightly, and social inventories were lightened for five consecutive weeks. Sales pressure fell, plus one quarter each. The economic data of this item are not ideal, making the market's expectation of the government's stimulus policies in the second quarter stronger, supporting the price at the bottom to a certain extent. It is recommended that downstream steel enterprises purchase on demand; traders make up the stock according to the amount of resources, and ship on rallies, and the operation of wet storage is the main operation; intermediate traders operate in short cycles. Pedestal Stand,Adjustable Plastic Pedestal,Adjustable Plastic Support,Plastic Pedestal Adjustment Jiangxi Taurus Technology Co., Ltd , https://www.chinapedestal.com

I. Domestic market dynamics 1. Changes in the domestic market Domestic building materials remained weak this month, but the decline was smaller than in February, including a slight increase in the price of thread in central China. The downstream startup was slow, and the accumulated social inventory in the previous period was still to be digested, which continued to restrict the steel prices this month. In March, it was the end of the quarter, and the financial pressure was originally higher than usual. In addition, the credit crisis related to the steel industry in the month was not unanswerable. The financial pressure of this month has become more prominent, so the majority of business operations during the month to **, so that the overall market continued to show a slow decline. The number of steel mills overhauled during the month has increased, and crude steel production has declined. With the gradual increase in temperature, terminal demand has begun to improve in the second half of the month, leading to a gradual weakening of the fundamentals in the second half of the year. The first-line resources in some markets have emerged. In addition, various economic data in the first quarter were not satisfactory, making the market's expectations for the government's stimulus policies in the second quarter to turn stronger. As a result, the market sentiment began to grow at the end of the month, and some cities witnessed rising trials.

2. Cost analysis There was a slight improvement in profit space this month. According to the cost model, as of March 31, domestic small and medium-sized steel enterprises 20mm three-tier rebar profitability of negative 471 yuan / ton, compared with the end of last month (negative 483) profit growth of 12 yuan / ton; 6.5mm high-line profitability space It was negative 355 yuan/ton, and the profit from the previous month (negative 389) was a positive increase of 34 yuan/ton. Since mid-December last year, the market price has dropped sharply for three consecutive months. The steel price is at historically low levels. There is limited room for further declines. The steady increase in the level of macroeconomic policy is expected to increase. In addition, during the peak season of traditional consumption, the market supply and demand may further improve. In April, steel prices may have some room for rebound. With regard to raw materials, demand will gradually improve, and market pressure on stocks will be reduced. In the short term, many steel mills and traders will need to make up the inventory, which will increase the turnover of the raw material market and strengthen the performance of raw materials. Taken together, the Building Materials Research Group expects that the profitability of small and medium-sized steel enterprises will improve by a certain margin this month.

3. Changes in total inventory of spirals The total inventory of domestic building materials fell sharply in March. As of February 28, total inventory was about 12.1085 million tons, an overall decrease of 8.49% compared with the previous month, an increase of 52.24% last month, a year-on-year decrease of 12.52%; of which total thread is about 9,574,100 tons, a decrease of 7.75% from last month, increased last month 51.04%, a year-on-year decrease of 10.63%; total wire rods were approximately 2,534,400 tons, a decrease of 11.19% compared with the previous month, an increase of 56.78% last month and a decrease of 19.00% year-on-year. According to the latest data from China Steel Association, in the middle of March, the country's crude steel was 16.9172 million tons, with an average daily output of 1691.7 thousand tons, and an increase of 31,200 tons of increase of 1.88%. Although destocking was effective, the crude steel production data was not very optimistic. In view of the start of demand, inventory was further digested. Considering comprehensively, it is expected that inventory will continue to decline in March, and the decline may be slightly slower than the same period of last year.

4. Import and Export Analysis (1) Import Analysis In February 2014, China's steel rod imports continued to decline in the same or a week-on-month ratio. Imports of wire rods totaled 34,700 tons, up 57.38% year-on-year, and up 42.48% month-on-month. Imports of rebars were approximately 0.26 million tons, down 4.8% year-on-year and down 23.91% month-on-month. In February, the total import volume of wire coils was approximately 37,000 tons, down 50.51% year-on-year and up 41.48% month-on-month. In March, the domestic building materials market was in a downturn, and the “golden three silver four†favorable market did not appear this year, and economic data in the first quarter was not Jia, the slow start of downstream demand, coupled with the excess supply of domestic steel mills, suppress steel prices rise. Due to insufficient domestic demand and low prices, steel mill imports have been suppressed. However, given that the market recovery has significantly accelerated over the beginning of the year, it is expected that the volume of imports will rise slightly in March.

(2) Export analysis In February 2014, China's exports of steel bars declined year-on-year, year-on-year increase, and wire rod exports both rose and increased month-on-month. Among them, exports of rebar were 6,200 tons, a year-on-year decrease of 74.29% and a month-on-month increase of 80%; wire rod exports were 582,700. Tons, up 18.77% and 867.22% respectively over the previous quarter. The total export volume of wire screw in February was approximately 587,900 tons, which was 14.43% and 824.86% higher than the previous month. In March, the international steel market operated steadily. The demand in the European market picked up. The steel mills raised their prices one after another and the market price was expected to increase. In the US market, the demand was obviously improved, and there was no preferential purchase for downstream purchases, and the price increased. Considered comprehensively, although China's steel prices have obvious advantages, Europe and the United States have gradually recovered their demand, and export conditions are favorable. However, anti-dumping investigations conducted by the United States on China's wire rod products cause the export volume to be compressed, and steel exports will not increase too much. It is expected that exports will increase slightly in March.

5. Downstream demand analysis (1) Infrastructure construction According to the latest data from the Ministry of Transport and the Bureau of Statistics, in February, transportation investment in fixed assets increased by -1.51%, a year-on-year increase of 19.24%, of which highways, inland waterways, and coastal construction investments were respectively Increase by 30.29%, -24.57%, -54.52%. In the same month, urban fixed asset investment increased by 17.9% year-on-year, construction project total investment increased by 16.8% year-on-year, total planned investment in new projects increased by 14.7%, and investment funds increased by 14.6%. It is believed that the growth rate of investment and capital in place in the first two months has slowed down compared to the same period of last year, but investment growth in new projects has been accelerating, and highway investment growth has been strong during the same period. This year, the state will strengthen the construction of comprehensive transportation networks such as railways and highways, improve the infrastructure of rural water circuit air letters, and increase the intensity of farmland water conservancy construction. It is expected that the construction of water conservancy, highways, and railways will accelerate in the short-term, and consumption of infrastructure steel such as spirals and pipe sections will rebound, and the recovery will be weak.

(2) Real-estate statistics released by the National Bureau of Statistics show that from January to February 2014, the national investment in real estate development reached 795.6 billion yuan, a nominal increase of 19.3% year-on-year, and the growth rate was 0.5 percentage points lower than that of last year; real estate development enterprise housing construction The area was 529,593 square meters, an increase of 16.3% year-on-year, and the growth rate was 0.2 percentage points higher than last year; the area of ​​new housing starts was 169.93 million square meters, down by 27.4%; the area of ​​housing completed was 12,418,000 square meters, down by 8.2%; real estate development enterprises The land purchase area was 40.62 million square meters, which was a year-on-year increase of 6.5%. The land transaction price was 100 billion yuan, an increase of 8.9%; the commercial housing sales area was 104.66 million square meters, a year-on-year decrease of 0.1%. Think that the first two months of the real estate market "cold and hot." The decline in sales of commercial housing and the tightening of funds, etc., have affected the start-up enthusiasm of housing companies, resulting in a significant drop in the area of ​​new housing start-ups. However, under the tightening of controls and the expected weakening of housing prices, housing enterprises have accelerated their construction, the construction conditions of the month are still acceptable, and urbanization and other potentials have become more visible. The strong demand has accelerated the speed of getting housing companies in hot-spot cities, resulting in a fiery land market. At present, the ** control of boots landing, "two-way control", classification guidance, protection of housing, shantytowns to make good profits, the first-line hot-spot city control is difficult to relax. In March, the overall transaction in the property market continued to decline, and the capital of housing enterprises was not optimistic. In the later period, the housing prices are expected to weaken, and the demand for commercial housing demand may be reduced. However, some housing enterprises will accelerate the promotion. It is expected that the real estate market will continue to recover from the seasonal weakness in the short term, and the demand for related building materials will slowly pick up.

6. Steel price adjustment analysis In March, the policy of steel mills was lowered. Under the macro-environment of sharp drop in period snails and related commodities and non-benefit of all parties, market prices continued to decline, and steel mills fell, and the difference in amplitude between different types of steel mills is quite different. Considering that most of the current market social stocks are still high, and demand It is difficult to improve the weak situation in the short term. It is expected that the policy of the steel mills will be stronger before the next month.

Second, ** market analysis 1. Technical analysis As of March 31, the main screw 1410 contract opening 3413, this month, the highest 3438, the lowest 3141, closing 3328, the closing price fell 84 from the previous month, a drop of 2.46%, turnover 48,184,696 hands. The end of the month is 1,885,346 lots.

From the technical analysis point of view, the 10-month moving average line of the May contract at the 10th of May was below the 10-month moving average to form a dead-fork; from the K-line perspective, the weekly K line oscillated at a low level, stabilized and recovered, and the trend indicator KDJ was running low. The leading indicator MACD was operating at Hongzhu interval; from the perspective of the Japanese K-line, the low level of the K-line rebounded, and the trend indicator KDJ diverged upwards, and the leading indicator MACD Hongzhu enlarged.

2. The outlook for the next month is expected to be 1410 during the first month of this month, with a narrower consolidation in the early part of the month, ranging from 3320-3370, with a slight correction in the later period. Next month, the bulls should participate properly in the early stage, and they should wait and see. The total positions of long and short positions are controlled within 10%, and the daily futures operation recommendations are specifically noted.

Third, the trend of the next month pre-judgment From the impact of the building materials market trends, the main factors, the next long and short odds are equal to: real estate financing is more difficult, even if the seasonal recovery of demand, its release intensity can only make businesses cautiously optimistic; March The inventory of steel mills continued to rise in the middle of the month, forcing factory price adjustments to be narrow, with limited impact on the market; raw material prices are expected to be weak and cost support is not good; however, economic data in the first quarter was rather sluggish, which may prompt macro-level steady growth policies to speed up the market. Zhengang City demand and business confidence; building materials, social inventories fell for five consecutive weeks, the current level is lower than the same period in previous years, sales pressure has slowed; therefore, the building materials research group expects the bottom of the market next month shock uplift, the extent is limited.